When global companies mistake U.S. expansion for a sales problem instead of an operational...

You can't hold leaders accountable if you don't give them visibility in their own market

Executive Briefing

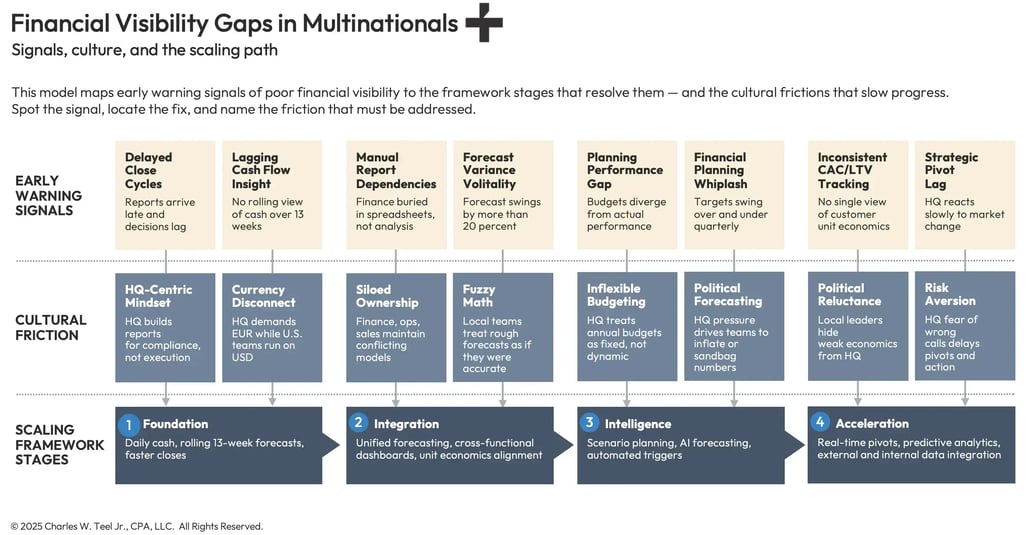

Multinational companies often believe they have visibility into U.S. operations through consolidated global reporting. In practice, those reports are backward-looking, formatted in headquarters’ currency, and stripped of the local insight required to manage performance. Without a U.S. P&L in dollars, department-level cost centers, or real-time variance tracking, accountability collapses. Managers are asked to deliver growth without the tools to connect decisions to outcomes.

The illusion of global oversight creates an overconfidence bias. Headquarters sees neat spreadsheets while U.S. leaders operate blind. The result is tactical firefighting: discounting to hit volume, delaying hires without savings, or defending numbers instead of leading teams. These blind spots appear consistently across subsidiaries—no cost-center visibility, revenue attribution errors, and missing variance analysis. Left unresolved, they erode margin, distort forecasts, and starve the U.S. of capital it could productively deploy.

The strategic risks are real. Blurred financials undermine forecasting accuracy, misallocate resources, and reduce board confidence. In one case, tens of millions were shifted to Europe because U.S. reports understated growth potential; by the time the error surfaced, competitors had already captured share.

Winning in the U.S. does not require new theory. It requires disciplined financial management applied locally: establish U.S. cost centers, deploy dashboards with variance analysis in USD, appoint U.S.-based financial leadership, integrate ERP with U.S. workflows, and tie budgets directly to commercial outcomes. These steps transform U.S. operations from tactical reaction to accountable management.

The U.S. is not a reporting line. It is the growth engine—and engines demand local visibility and financial command.

YOU CAN'T MANAGE WHAT YOU CAN'T MEASURE. That truth is old, but the problem is real. In leadership conference rooms from Frankfurt to Tokyo, headquarters executives assume they know how the U.S. business is performing. The month-end package arrives, rolled up in global formats, and the numbers appear tidy. Yet when results disappoint, the same question comes back from HQ: “Why is the U.S. not delivering?”

Now picture the scene. A dozen executives sit around a polished table. Slides flash across the screen, but every chart is denominated in Euro. The U.S. team is asked to explain missed targets with no local P&L in U.S. Dollars, no departmental budget comparisons, and no variance analysis. The local GM knows demand has shifted, margins are tightening, and headcount costs are rising.

But when the numbers are translated into global reporting lines, none of that nuance comes through. It is like being asked to explain American results in a foreign language. If you want to connect with regional leadership, you must speak in their local currency. Without that baseline, accountability is meaningless. And when accountability breaks down, performance quickly follows.

The Illusion of Global Consolidation

Month-end consolidation is tidy but misleading. It tells the story of what has happened, not what is happening. By the time HQ reviews its package, U.S. leaders are already a month behind the curve.

The danger lies in the illusion of control. Headquarters sees uniform tables across markets and assumes comparability equals precision. The spreadsheets are formatted identically, full of percentages carried to two decimal places. Yet they omit the ground-level view of which products are bleeding margin, which customers are unprofitable, or which departments are running over budget. The orderliness fosters a false sense of precision, creating an overconfidence bias built on data that is partial at best.

Here is the fact: U.S. managers are operating without visibility. No local P&L in USD. No real-time margin tracking. No departmental budget view. Headquarters believes it has oversight, but leaders charged with execution are making decisions in the dark. This is not a system glitch. It is a discipline gap. If leadership mistakes consolidation for oversight, accountability collapses—and what follows is the accountability gap that drags performance down.

The Accountability Gap

Accountability follows visibility. Take away visibility and accountability collapses.

In U.S. subsidiaries, managers often carry revenue targets without the authority to manage costs. They are tasked with delivering sales growth but lack the ability to trace spending to cost centers or tie commercial actions to financial outcomes.

The result is reactive choices. One U.S. general manager resorted to deep discounting to hit quarterly revenue, unaware that each sale wiped out gross margin. The target was met, but profitability collapsed. Another delayed critical hires to show “discipline,” but because the costs were already embedded in overhead, the decision only hurt capacity while savings never materialized. These are tactical moves, not strategic management.

When managers are denied transparency, they cannot own performance. It is not avoidance. It is structural. And those blind spots show up in the same three ways, every time. Which takes us directly to the reporting failures that repeat across nearly every U.S. subsidiary. U.S. managers are not resisting accountability — they are often operating without the time, tools, or political authority to connect decisions to outcomes.

Common Reporting Gaps

The same failures appear in most multinational U.S. subsidiaries:

- No department-level visibility. Without cost-center reporting, marketing cannot measure ROI, operations cannot track overhead, and sales cannot connect cost to acquisition.

- Revenue attribution errors. Cross-border transactions skew topline results, leaving U.S. leaders accountable for revenue they never controlled.

- No variance tracking. Without budget versus actual comparisons in USD, variances go unnoticed until HQ sees the consolidated miss.

These are not technical limitations. They are management choices. Until they are fixed, U.S. operations will continue to run on instinct rather than financial command. Left unresolved, these failures do more than frustrate managers. They put the company itself at risk. And once reporting gaps harden into blurred financials, the consequences escalate into enterprise-level risks that erode forecasting, resource allocation, and board confidence

Strategic Risk of Blurred Financials

Poor financial visibility in the U.S. is more than an operational nuisance. It creates enterprise risk.

-

Forecast inaccuracy. Without reliable inputs, forecasting becomes educated guessing.

-

Misallocation of resources. Capital is shifted away from U.S. opportunities based on incomplete data, starving a high-return market.

-

Erosion of board confidence. Directors see repeated U.S. shortfalls and interpret them as a lack of discipline, undermining credibility far beyond one region.

The cost of misallocation is rarely visible until much later. One multinational shifted tens of millions to a European unit because U.S. reports understated growth potential. By the time the error was discovered, competitors had already gained share in the American market. The decision was rational given the data HQ saw. The problem was that the data excluded the local financial signals that would have justified expansion in the U.S. I once sat with a U.S. GM who learned only at quarter-end that his fastest-growing customer was unprofitable — obvious in USD, invisible in Euro.

Another finance lead confided that she spent more time defending numbers to headquarters than leading her team. That imbalance was not a performance issue, it was a structural flaw. The lesson is simple: blurred numbers do not just hurt reporting. They distort strategy. And distorted strategy leads directly to missed opportunities. Which is why disciplined financial management practices must be applied locally.

U.S. Financial Management Best Practices for Multinationals

Winning in the U.S. does not require new theory. It requires financial discipline applied locally. The companies that succeed follow consistent procedures.

- Establish U.S. cost centers with budget ownership.

Give managers responsibility for their spend. When marketing owns its budget and operations owns overhead, accountability becomes specific. HQ can also see which functions are efficient and which need restructuring. Without this step, accountability has no anchor. - Deploy localized dashboards with variance analysis (in USD).

Stop relying on HQ spreadsheets. U.S. leaders need to see budget versus actuals in real time, in their own currency. Dashboards designed for USD expose cost overruns or margin erosion early, when corrections are possible. This is the difference between proactive management and damage control. - Appoint U.S.-based financial leadership.

A controller or fractional CFO in-market turns strategy into execution. Remote oversight cannot substitute for leaders embedded in local operations. These professionals ensure U.S. managers make decisions with financial discipline, not instinct. In practice, this often means identifying risks weeks earlier than HQ would ever see them. - Integrate ERP with U.S. workflows.

Global systems must adapt to U.S. business practice. When ERPs are harmonized, revenue attribution errors decline and HQ finally gets apples-to-apples comparisons. Integration is not about compliance. It is about creating a common language between headquarters and the U.S. team. That shared language builds trust and accelerates corrective action. - Tie budgets to commercial outcomes.

Make the connection explicit: margin by product, cost per acquisition, return on capital. Every U.S. manager should see how their decisions shape financial performance. This closes the loop between financial management and commercial execution. When incentives and accountability align, performance accelerates.

Together, these measures move U.S. subsidiaries from tactical reaction to accountable management. When accountability becomes routine, growth turns from aspiration into repeatable performance — the very outcome headquarters expects but rarely achieves without local visibility.

Strategic Insight

Financial visibility is not about generating reports. It is about linking action to outcome.

A U.S. subsidiary without localized financial management is not underperforming. It is under-led.

Executives who view the U.S. as a line on a consolidation package will continue to be surprised. Executives who treat the U.S. as a market with real budgets, accountable leaders, and disciplined financial tools will see stronger revenue, higher margins, and renewed board confidence.

The U.S. is not a reporting line. It is your growth engine. And engines do not run on global spreadsheets. They run on financial command, in-market, in real time, in U.S. Dollars.

References

The insights in this article are drawn from the author’s direct observations, data analysis, and strategic findings across client engagements at Teel+Co, as well as his prior corporate experience as a senior financial leader in mid-market companies.

Copyright © 2025, Charles W. Teel Jr., CPA, LLC. All Rights Reserved.